The university budgeting system is complex and the SDC funding scenario is equally so. While the administrative manager is responsible for the handling and oversight of funding matters on a day-to-day basis, BPPM 70.03 states the department chair (director) is responsible for ensuring that all expenditures incurred by accounts under his or her authority are for appropriate and legitimate purchases. This document is intended, in part, to inform the director of best practices and to assist the program heads and others who may be granted budget authority as to how to spend. While such a document may be particularly helpful in a budget crunch, it is intended to be guideline to follow at all times.

WSU uses fund accounting, also known as “bucket accounting.” The source of funds determines the bucket it goes into. The SDC uses four buckets:

- State appropriated funds; also known as “Permanent Budget Line” or “PBL.” The SDC can receive PBL for both salaries and operations. Each year, after the SDC working budget is completed, the director should work with the administrative manager to allocate a portion of the remaining PBL for general and administrative expenses (G&A), for faculty & professional development; for each program; for marketing/recruitment; for the gallery; for computers/IT; and for the shops. (Fund type 001, Program 06)

- The G&A fund may be used for:

- Major instructional support

- Adjunct faculty to teach a required class

- Accreditation costs (including travel)

- Membership fees necessary to maintain accredited status

- Office expenses including supplies and copy machine contracts.

- SDC-wide instructional support

- Ancillary activities related to SDC courses not currently in course fees

- Multi-disciplinary activities related to SDC courses not in course fees

- Travel and events related to SDC Central Board meeting

- Major instructional support

The program allocations may be used for:

- Ancillary instructional support, such as:

- Teaching assistant-type support for courses not already in SDC budget forecast

- Software/computer/printing needs for courses that extend beyond regular fees, including time-slip employees to help

- Travel/lodging needs for courses or site visits that extend beyond course fees

- Study tours beyond fees (such as extra rooms in the hotel);

- Faculty workshops

- Student conference or workshop travel

- Faculty travel extending beyond the $1,500 or beyond the start-up fund related to travel (if negotiated)

*For additional information, see the Allowable Purchases (By Program) table 1 below for Program 06.

2. Self-sustaining funds (such as course fees). The SDC generates revenue in the form of course, shop, and computer fees. These dollars are only to be used for the courses that have them. (Fund type 148, Program 06)

*For additional information, see the Allowable Purchases (By Program) table 1 below for Program 06.

3. Grant funds (restricted). Grant money is awarded for a specific purpose and must be expended for that purpose within the established time frame. (Fund type 145, Programs 11-14)

*For additional information, see the Allowable Purchases (By Program) table 1 below for Programs 11-14.

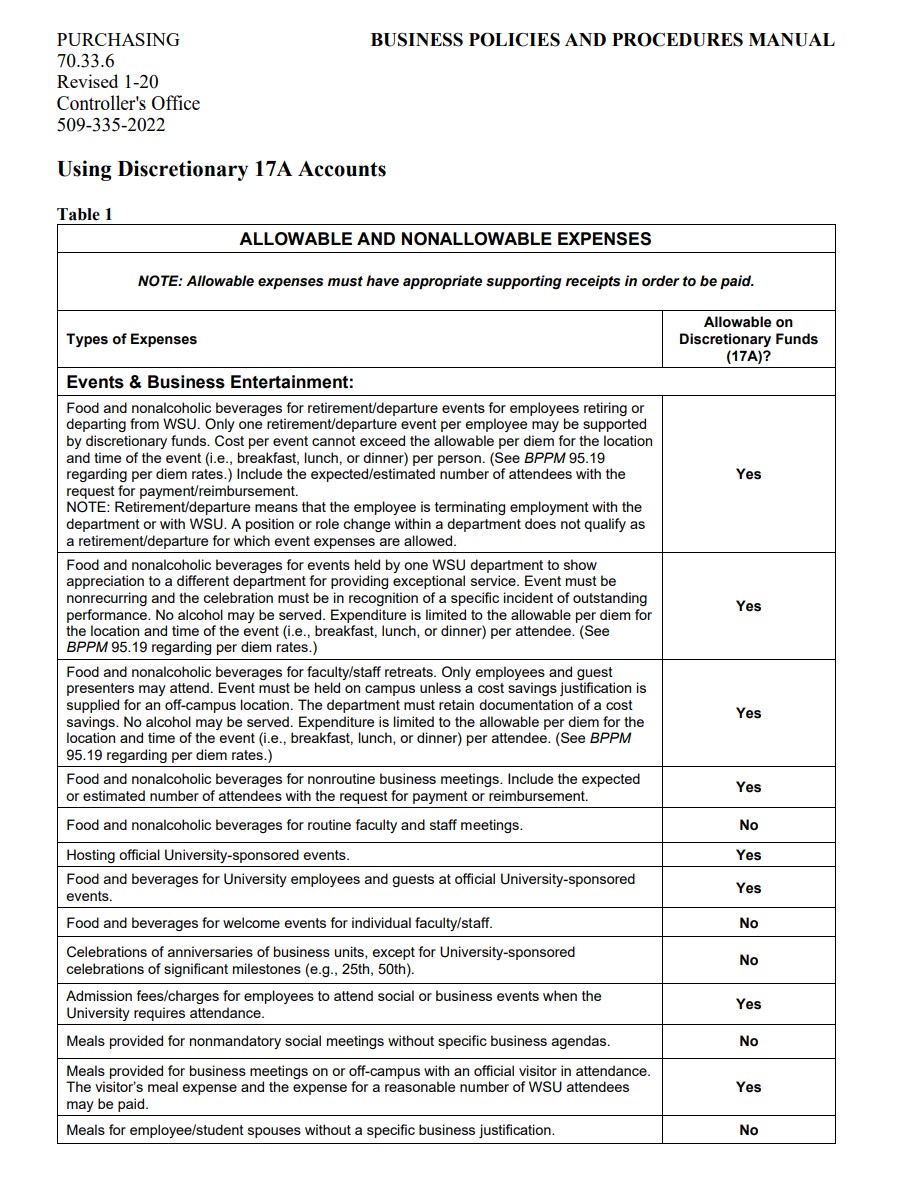

4. Discretionary funds, known as 17A funds. Such funds must be spent according to the Gift Use Agreement (GUA), and must be accounted for in reports to alumni (e.g. thank you letters) and any audits that may be requested by university officials or donors. All purchases must be legal and meet the test of public scrutiny for appropriateness. (Fund type 846, Program 17)

- The 17A funds may be used for:

- Big program-related development (such as program-specific facilities or equipment)

- Fees for non-required courses (e.g., electives, summer courses). This could include paying faculty or instructor’s additional salary or time slip.

- Food for events

- 17A funds must not be used for:

- Purchases, which conflict with donor’s stated desires.

*For additional information, see the Allowable Purchases (By Program) table 1 linked below.

*For a breakdown of whether or not a purchase is allowable with a 17A account, see the Using Discretionary 17A Accounts tables 2-6 linked below.